Talk to our experts

Loan approval timelines are one of the most direct reasons/drivers of borrower drop-off in banking. When the process takes too long, applicants move on, often to a digital-first lender who returns a decision in hours rather than days. For banks still running on outdated loan origination system software, that speed difference is lost revenue, not just a process inefficiency.

If your lending operations team is managing origination through a combination of spreadsheets, email threads, and manual data entry across disconnected systems, this is not unusual. Most institutions that struggle with the loan origination system (LOS) software performance are not operating outdated workflows because they lack awareness. They are operating on them because replacing a system that touches compliance, credit risk, customer data, and regulatory reporting simultaneously is genuinely complex, and the cost of a misstep during transition is high. The pressure to modernize is real, and so is the pressure to get it right.

In this article, we explore what a loan origination system is, the key challenges financial institutions face in origination today, and how OutSystems, a leading low-code development platform, enables organizations to build, customize, and deploy LOS solutions faster and with greater flexibility than traditional development approaches allow.

What is a loan origination system (LOS) and how does it work?

A loan origination system (LOS) is a software platform that automates and manages the end-to-end loan origination process for financial institutions such as banks, credit unions, and mortgage lenders. It serves as a central hub for all activities related to loan applications, approvals, and disbursements. It replaces the fragmented chain of manual steps and disconnected tools that characterize legacy origination with a single governed workflow where each stage is tracked, documented, and auditable.

LOS in banking creates consistency where every application follows the same process, every compliance checkpoint is enforced at the same point in the workflow, and every credit decision is recorded with the documentation required to support it. That consistency is what allows institutions to scale origination volume without proportionally scaling their operations teams, and to satisfy regulatory examiners who require a clear, defensible record of how lending decisions were made.

Whether you are evaluating a commercial loan origination system, a mortgage loan origination software, or a consumer lending software for retail banking, the core objective is the same: replace manual, error-prone workflows with a governed, automated process that scales with your business.

The seven steps of a loan origination process

A typical loan origination process for any lending institution (banks, credit unions, micro-finance institutions, etc) consists of seven steps. This includes qualification, documentation, application processing, underwriting, credit decision, quality check, and loan approval & disbursement. Let’s discuss these steps in detail below:

- Borrower Pre-Qualification The borrower submits basic identity, employment, income, and loan purpose details for initial eligibility screening.

- Documentation The borrower completes a formal application and submits supporting financial and employment documents, online or offline.

- Application Processing The credit department validates submitted information for accuracy and completeness, running algorithmic analysis to assess repayment capacity.

- Underwriting Creditworthiness is assessed against credit history, debt-to-income ratio, and repayment capacity to determine approval, denial, or conditional modification.

- Credit Decision A final decision is issued. Denied applications may be reconsidered with adjusted terms. Files requiring additional information are returned to the originator.

- Quality Check The application is reviewed for regulatory compliance and adherence to internal policies before final approval.

- Loan Approval and Disbursement Once terms are agreed, the loan is disbursed via bank transfer, cheque, or digital channels. End-to-end, this loan origination process typically takes months manually, creating significant paperwork and operational overhead at every stage.

| DIMENSION | MANUAL PROCESSING | MODERN LOS SOFTWARE |

|---|---|---|

| Application intake | Paper forms, email, and branch visits | Digital self-service portal, mobile-first onboarding |

| Document collection | Manual requests, email attachments | Automated checklist with OCR-based verification |

| Credit assessment | Analyst-led, time-intensive | Automated bureau pulls, rules-based decisioning |

| Approval timeline | Multiple business days, variable | Faster, more consistent decision-making |

| Compliance tracking | Manual audit trail, error-prone | Automated audit logs, real-time regulatory flag alerts |

| Human error risk | High, particularly in data entry | Significantly reduced through workflow automation |

| Scalability | Limited by headcount | Scales with application volume without proportional staffing increases |

| Customer experience | Fragmented, opaque, high abandonment risk | Transparent status updates, self-service visibility |

| Data integrity | Inconsistent across systems | Single source of truth with integration to core banking |

What Role Does AI Play in Modern Loan Origination?

AI is moving from pilot projects into production across automated loan origination systems, covering document processing, credit decisioning, and fraud detection at institutions that have committed to the investment. Its practical impact spans four areas.

Faster and Smarter Data Processing: AI scans financial documents, application forms, and transaction histories, extracting and classifying relevant information with precision and speed. This reduces human error at the data intake stage and accelerates the path to a credit decision considerably.

Enhanced Credit Scoring: Traditional credit scoring relies on a limited set of factors: credit history, income, and debt levels. AI-driven models expand this by incorporating alternative data sources such as utility bills and real-time financial behavior, producing more accurate assessments, particularly for thin-file borrowers with limited credit history.

Fraud Detection and Risk Mitigation: Machine learning algorithms identify unusual patterns in applicant data that indicate potential fraud, such as discrepancies between reported and actual income or synthetic identities created to bypass credit checks. This continuous monitoring reduces fraud exposure without slowing down legitimate applications.

Improved borrower-facing responsiveness Customer Experience: AI-powered chatbots and virtual assistants guide borrowers through the application process, answer queries, and provide real-time status updates. For institutions competing against fintech lenders on the digital lending platform experience, this layer of responsiveness matters operationally, not just as a feature.

Mashreq Bank (UAE) automated its customer onboarding process using AI and ML-based OCR technology, replacing manual document verification with automated extraction and validation workflows, reducing processing time substantially while improving data accuracy.

Challenges in LOS and how OutSystems addresses them

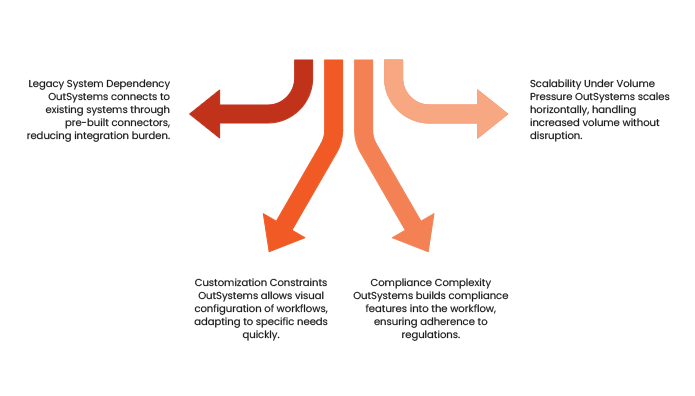

Most banks and lenders do not struggle with loan origination because they lack awareness of better options. They struggle because the path from legacy systems to a modern digital loan origination system is genuinely difficult. Here are the four most common challenges and how OutSystems addresses each one.

1. Legacy System Dependency: Core banking systems at many institutions were not designed to support modern API-based integrations. LOS integration with existing infrastructure requires significant custom development, which traditional software approaches make slow and expensive. Integration failures are the single most common reason LOS implementations run over time and budget.

How OutSystems addresses this: OutSystems connects to core banking systems, credit bureaus, CRM platforms, and third-party verification services through pre-built connectors and a flexible API layer. This reduces the loan origination system integration engineering burden considerably and keeps implementation timelines on track.

2. Customization Constraints: Off-the-shelf loan origination solutions rarely fit an institution’s workflows out of the box. Customizing them through traditional development cycles takes months and creates maintenance overhead that compounds over time. Every regulatory change or new product launch becomes a development project.

How OutSystems addresses this: Teams configure and modify LOS workflows visually, adapting the system to their specific origination process without writing code from scratch. When compliance requirements change or new loan products need to go live quickly, the turnaround is measured in days rather than months.

3. Compliance Complexity: US lenders must address Equal Credit Opportunity Act (ECOA) adverse action requirements (documenting the specific reasons a loan was denied), Home Mortgage Disclosure Act (HMDA) reporting (tracking loan data by geography and demographics), Community Reinvestment Act (CRA) compliance, and state-level disclosure rules, simultaneously. Any LOS application that does not account for these from the start will require costly rework.

How OutSystems addresses this: OutSystems builds audit trails, role-based access controls, and regulatory reporting modules directly into the origination workflow rather than adding them after deployment, which is where compliance risk most commonly originates. The platform also supports Know Your Customer (KYC) and Anti-Money Laundering (AML) requirements natively.

4. Scalability Under Volume Pressure Origination volumes fluctuate with interest rate cycles, seasonal demand, and market conditions. Institutions running on rigid infrastructure struggle to scale up during peak periods without high cost or operational disruption.

How OutSystems addresses this: OutSystems applications scale through horizontal scaling (adding server capacity without rebuilding the application), allowing institutions to handle increased volume without a full platform rebuild. A cloud-based loan origination system deployment further supports consumption-based scaling that aligns capacity to actual origination demand.

Credit Bureau Singapore built a centralized Debt Consolidation Registry Portal used by major banks across the country. The portal enables loan officers and registry administrators to manage and verify debt consolidation records against Monetary Authority of Singapore guidelines, replacing a manual process that previously ran across multiple disconnected institutions.

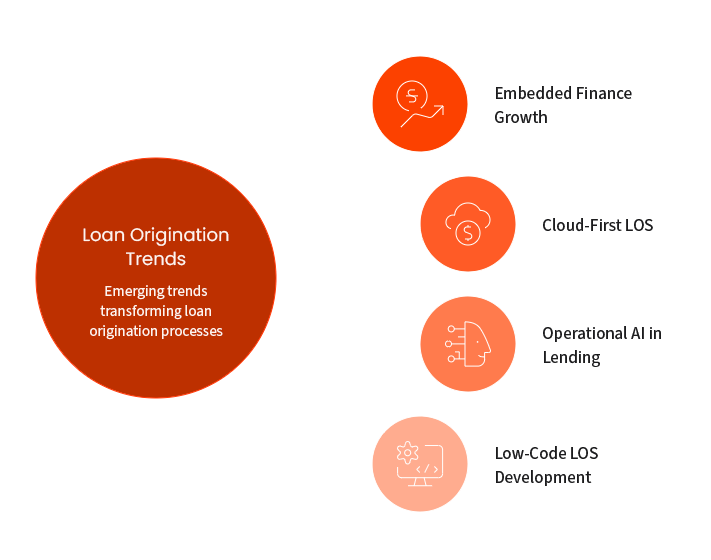

Key Trends Shaping LOS in 2026

Embedded finance growth: Lending is no longer confined to bank portals and branch applications. Buy Now Pay Later at checkout, working capital lines integrated into accounting software, and instant credit at point-of-sale all require a loan processing automation infrastructure capable of operating via API at speed and scale. Lenders whose origination systems cannot support API-first product delivery will find themselves locked out of these channels as they grow.

Cloud-First LOS: On-premise LOS deployments face longer upgrade cycles, higher infrastructure maintenance costs, and limited ability to scale during peak periods. Cloud-based loan origination systems offer configurable deployment and consumption-based scaling that on-premise architecture cannot match. On-premise retains relevance primarily for institutions with regulatory restrictions on cloud data residency.

Operational AI in lending: AI applications in automated loan origination have crossed from pilot projects into production at institutions that have made the investment. Document processing, credit scoring, and fraud detection are the three areas where AI is delivering measurable operational improvements today.

Low-Code LOS Development: Traditional LOS system implementations take months, create long-term maintenance overhead, and require large development teams to modify. Low-code platforms like OutSystems allow financial institutions to build, modify, and deploy loan origination software with smaller teams and shorter time to production. For institutions that need to respond quickly to regulatory changes or new product requirements, this is a structural advantage over traditional development approaches.

Loan Origination System Use Cases with OutSystems

Consumer Lending. A retail bank uses OutSystems to build a mobile-first consumer lending software portal where borrowers apply, upload documents, and receive decisions without branch visits. The workflow connects directly to credit bureaus and the core banking system, eliminating manual data re-entry at every stage.

Commercial Loan Origination. A mid-size bank builds a commercial loan origination system on OutSystems that handles financial statement spreading, multi-borrower structures, and covenant tracking within a single governed workflow. Loan officers manage the full loan pipeline from application to approval in one interface.

Regulatory Compliance Automation. A financial institution uses OutSystems to configure ECOA adverse action notices, HMDA reporting, and CRA tracking directly into the origination workflow, removing the manual compliance layer that previously required a dedicated team to manage.

How Ranosys can help you modernize loan origination:

Getting a loan origination system software modernization program right requires more than selecting a platform. It requires mapping current workflows accurately, identifying integration dependencies with core banking and compliance systems, and sequencing the implementation to avoid disrupting active lending operations.

Ranosys has worked with financial institutions across banking, credit, and financial services globally, including Mashreq Bank (UAE), Ahli United Bank (Kuwait), HDFC Bank (India), OCB Orient Commercial Joint Stock Bank (Vietnam), Credit Bureau Singapore, Experian, and Ford Motor Credit Company (US), delivering technology implementations that span digital onboarding, workflow automation, mobile banking, and compliance portal development.

As a certified OutSystems partner, Ranosys designs and delivers LOS programs that fit your institution’s actual origination complexity. Our services cover:

- Current-state workflow assessment and analysis

- LOS design and development on OutSystems

- Loan origination system integration with core banking platforms, credit bureaus, and CRM systems

- Compliance rule implementation and audit trail configuration

- Data migration and parallel-run testing

- Post-launch optimization and performance monitoring

Vikas Sharma

Senior System Analyst

OutSystems Champion and Solution Architect with 14 years of IT experience and 8 years of deep expertise in OutSystems. Certified across multiple OutSystems technologies, specializing in enterprise architecture, integrations, and scalable low-code solutions. Connect with him on Linkedin.